Discover how Stripe grew from a small startup into a global fintech leader, powering online payments, marketplaces, and financial infrastructure for millions of businesses including Shopify, Amazon, and Lyft across 45+ countries.

Discover how Stripe grew from a small startup into a global fintech leader, powering online payments, marketplaces, and financial infrastructure for millions of businesses including Shopify, Amazon, and Lyft across 45+ countries.

Image courtesy of huskysnow82.medium

In just over a decade, Stripe has transformed from a startup tackling payment complexity into one of the most influential fintech companies in the world. With a developer-first approach, a modular suite of financial tools, and an unwavering focus on global scalability, Stripe has become the financial infrastructure of choice for millions of businesses, from startups to global tech giants. This article explores Stripe’s journey, its core products, and its vital role in shaping the future of digital finance.

Stripe is one of the world’s leading fintech companies, known for revolutionizing online payments infrastructure for internet businesses. Here's a detailed breakdown of what Stripe is, how it operates, and why it’s considered a major player in the global fintech ecosystem:

The Fintech Sector in the U.S.

As of 2024, the U.S. fintech market is valued at over $4 trillion in transaction value (Statista). The U.S. is home to over 10,000 fintech startups, the most in the world. Venture capital investment in U.S. fintech companies hit $25–30 billion per year in recent cycles (though slightly down from the 2021 peak).

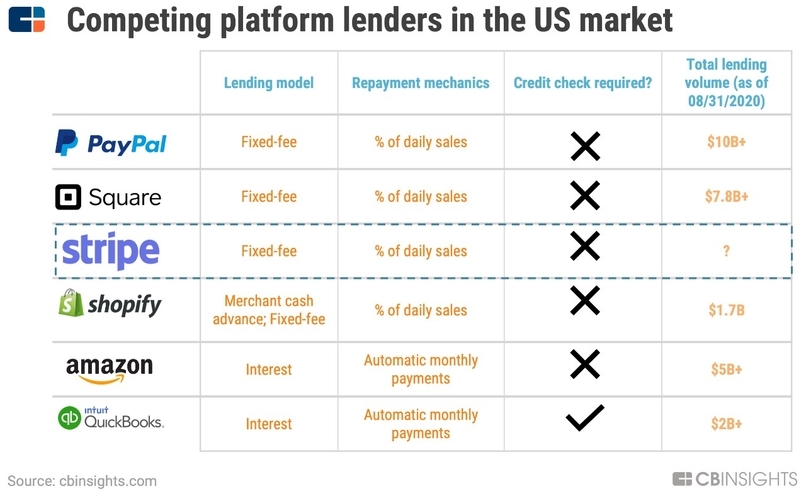

Digital Payments: PayPal, Stripe, Square (Block), Apple Pay. Growth driven by mobile payments, P2P transfers, and e-commerce. Increasing adoption of BNPL (Buy Now, Pay Later) models — e.g., Affirm, Afterpay.

Neobanking & Challenger Banks: Digital-first banks like Chime, Varo, Current, SoFi. They offer lower fees, mobile-first experiences, and faster access to paychecks. Some are FDIC-insured, others partner with chartered banks.

Robo-Advisors & Investment Apps: Platforms: Robinhood, Betterment, Wealthfront. Democratized stock trading and investing for Gen Z & millennials. Increased regulatory scrutiny after GameStop saga and meme stocks.

Lending & Credit: Key players: LendingClub, Upstart, Prosper. Use of AI and big data to evaluate creditworthiness. Expansion into SME lending, auto loans, and student loans.

Insurtech: Notable names: Lemonade, Hippo, Root Insurance. Use AI/ML to underwrite policies more efficiently. Focus on home, renters, and auto insurance with lower operating costs.

Blockchain & Crypto: Major hubs: Coinbase, Kraken, Gemini. Regulated crypto exchanges and wallet platforms. NFT marketplaces, DeFi platforms, and increasing institutional crypto adoption (e.g., BlackRock and ETFs).

Top Fintech Hubs in the U.S. San Francisco / Silicon Valley – epicenter of fintech innovation (Stripe, Plaid, Square). New York City – traditional finance meets fintech (Betterment, OnDeck). Chicago – payments and trading tech. Atlanta – “Transaction Alley,” strong in payment processing (Fiserv, Global Payments). Miami & Austin – fast-emerging crypto and blockchain hubs.

Regulation & Compliance SEC, OCC, FINRA, CFPB, FDIC – agencies regulating fintech depending on the activity. Fintech firms face growing scrutiny on: Data privacy. KYC/AML (Know Your Customer / Anti-Money Laundering). Consumer protection. Crypto asset classification

Trends & Future Outlook. Embedded Finance – offering banking services within non-financial platforms (e.g., Shopify offering loans to merchants). AI-driven personalization – smarter robo-advisors, fraud detection, and credit scoring. Financial inclusion – targeting underbanked Americans. Cross-border fintech expansion – U.S. startups entering LATAM, Southeast Asia, etc. CBDC debates – discussions around a U.S. digital dollar.

Stripe was founded in 2010 by Irish brothers Patrick and John Collison, who recognized a fundamental problem: online payments were unnecessarily complicated and difficult for developers. Their mission was to simplify payment processing through clean APIs and developer-centric design. Backed by Y Combinator and investors like Peter Thiel and Elon Musk, Stripe launched publicly in 2011 and quickly attracted innovative startups that were also building the next generation of internet services.

Headquarters: San Francisco, California, USA (with a dual HQ in Dublin, Ireland). Employees: ~7,000+ globally. Valuation (2024): ~$50–60 billion (private company). Status: Private (but IPO rumors continue)

Here is a detailed history and growth story of Stripe, from its humble beginnings to becoming one of the world’s most influential fintech giants:

Patrick Collison and John Collison, two Irish brothers and programming prodigies. Both were previously known for creating Auctomatic, an auction management system for eBay sellers (sold for ~$5 million in 2008).

While living in Silicon Valley, the brothers noticed that accepting online payments was extremely difficult for startups: Developers had to integrate with legacy systems (like PayPal or banks). Setup was complex, slow, and full of compliance roadblocks.

“We wanted to make it as easy to accept payments as it is to launch a web app.” — Patrick Collison

Initially called /dev/payments in 2010. Rebranded as Stripe in 2011. Backed by Paul Graham and Y Combinator — YC gave them $20K in seed funding. Quickly attracted attention from Elon Musk, Peter Thiel, and Sequoia Capital.

2011: Official public launch. Stripe differentiates with: Simple API and clean documentation. Instant setup, no merchant account needed. Developer-first approach

2012–2014: Gains traction with startups: Shopify, Lyft, Postmates, Kickstarter. Raises Series A and B rounds led by Sequoia and Peter Thiel’s Founders Fund. By 2014, processing billions in payments annually.

Global Expansion & Product Diversification (2015–2019)

2015: Expands beyond the U.S. into Europe, Australia, and Asia. Launches Stripe Atlas – allowing global founders to incorporate U.S. companies remotely.

New Products: Stripe Connect (2015): For marketplaces and platforms (e.g., Uber, Airbnb). Radar (2016): Built-in fraud detection. Billing & Subscriptions: Enables recurring payments and invoicing. Terminal (2018): Hardware + software for in-person payments.

Developer Ecosystem: Stripe positions itself as the “AWS for payments” — offering a suite of APIs for money movement, from card processing to identity verification.

COVID-19 Acceleration (2020): E-commerce and remote services boom. Stripe usage surges across industries: education, healthcare, logistics, remote work platforms. Launches Stripe Climate to fund carbon removal projects.

Fundraising Milestones: 2012 Series A $100M, 2016 Series D $9B, 2020 Series G $36B, 2021 Series H $95B (peak valuation). Stripe becomes America’s most valuable private fintech.

Major Clients (by 2022): Amazon, Shopify, Google, Zoom, Notion, Instacart, Salesforce, Atlassian, Slack, Lyft and thousands of startups and online marketplaces.

New Product Launches: Stripe Issuing – issue branded debit/credit cards via API. Stripe Treasury – embedded banking-as-a-service (partnering with Goldman Sachs, Barclays). Tax – automates global sales tax and VAT compliance. Identity – for identity verification/KYC. Financial Connections (2022) – open banking APIs.

Global Focus: Opens major offices in Dublin, Singapore, Tokyo, London, Dubai. Expands into Brazil, UAE, India — key high-growth markets.

Regulatory and Competitive Landscape: Increased regulatory scrutiny globally (AML, crypto, data privacy). Rising competition from PayPal, Square, Adyen, Checkout.com, Braintree. Pressure to go public amid market volatility.

Patrick and John Collison have expressed that Stripe's mission is to increase the GDP of the internet by enabling more businesses to start, scale, and thrive online. Deeper AI integration (fraud, identity, insights). More tools for embedded finance. Ongoing potential for IPO or direct listing. Likely expansion into credit, lending, and cross-border finance infrastructure.

Stripe provides financial infrastructure for the internet, allowing businesses to: Accept online and in-person payments. Manage subscriptions and invoicing. Handle fraud prevention. Issue virtual and physical cards. Enable bank transfers and payouts. Its products are widely used by e-commerce sites, SaaS companies, marketplaces, and mobile apps.

Global Reach: Operates in over 45+ countries. Supports 135+ currencies. Major markets: U.S., Canada, U.K., EU, Singapore, Australia, Japan, Brazil, UAE

Technology Focus: API-first and developer-centric. Integrates easily with platforms like Shopify, WooCommerce, Wix, Salesforce, NetSuite. Enables custom payment flows for startups to Fortune 500s

Business Model: Primarily transaction-based fees. Example: ~2.9% + $0.30 per successful card charge in the U.S. Also earns from value-added services like fraud protection, card issuance, and international conversion.

Stripe’s Competitive Edge: Ease of integration. Global compliance built-in (KYC/AML). Scalable for startups to enterprises. Extremely developer-friendly API and documentation. Constant product innovation (crypto payments, embedded finance, open banking)

Recent Developments: AI investment: Stripe is integrating AI to optimize fraud detection, user experience, and API performance. Enterprise push: Increasing focus on big enterprise clients and regulated financial services. Partnerships: Collaborates with Goldman Sachs, Barclays, Citibank, and JPMorgan for infrastructure.

Compliance & Regulation: Stripe is not a bank, but partners with regulated banks to offer financial services. Ensures PCI-DSS compliance, GDPR readiness, and AML/KYC regulations across regions. Helped democratize access to online payments, especially for small startups and global entrepreneurs. Considered one of the most influential fintechs in shaping the digital economy. Drives embedded finance, allowing non-financial companies to integrate financial services seamlessly.

Stripe grew rapidly by solving a core pain point for online businesses: the need for seamless, scalable, and global payment infrastructure. By 2014, it was processing billions in payments annually. Between 2015 and 2020, Stripe expanded globally, launched new products such as Connect, Radar, and Terminal, and cemented its reputation as the “AWS of payments.”

The COVID-19 pandemic only accelerated its growth. With businesses rushing to digitize, Stripe became the go-to solution for online payments. By 2021, Stripe reached a $95 billion valuation, making it the most valuable private fintech company in the U.S.

Stripe’s suite of products offers more than just payment processing:

The foundational product that allows businesses to accept online and in-person payments in over 135 currencies securely and globally.

Key Features: Supports credit/debit cards, wallets (Apple Pay, Google Pay), bank debits (ACH, SEPA), and more. Accepts payments in 135+ currencies with automatic currency conversion. Built-in fraud protection (Radar) and compliance (PCI-DSS). Tools for subscriptions, one-time payments, marketplaces, and global payout support. Localized payment methods — e.g., iDEAL (Netherlands), FPX (Malaysia), Alipay (China).

Ideal For: E-commerce stores, SaaS platforms, apps, and international businesses.

Enables platforms and marketplaces like Shopify, Lyft, and Upwork to onboard and pay third-party sellers, drivers, or freelancers. Designed for platforms and marketplaces to pay out to third-party sellers, vendors, or service providers.

Key Features: Instant or scheduled payouts to sellers in 35+ countries. Onboards users with KYC-compliant workflows. Handles complex flows like split payments, platform fees, and tax collection. White-label or branded onboarding experience.

Example Use Cases: Uber paying drivers. Shopify paying merchants. Kickstarter distributing funds to project creators

Helps global founders incorporate U.S. companies, obtain bank accounts, and manage legal and tax paperwork. A toolkit that helps entrepreneurs start a global business from anywhere, especially in the U.S.

Key Features: Incorporates a U.S. Delaware C-Corp in days. Provides a U.S. business bank account (in partnership with Mercury/others). Issues tax ID (EIN) and handles IRS documentation. Offers legal templates (founder agreements, IP assignment). Access to Stripe’s startup legal & tax guidance.

Ideal For: Startups, founders outside the U.S., SaaS businesses targeting a global audience.

A powerful fraud detection system that uses machine learning to block suspicious transactions in real time. A built-in fraud detection and prevention system, powered by machine learning.

Key Features: Blocks fraudulent transactions in real-time. Learns from billions of data points across Stripe’s global network. Custom rules and risk scores per transaction. Includes 3D Secure, device fingerprinting, behavioral analysis. Integrated with Payments by default, no extra setup.

Ideal For: High-risk or high-volume businesses wanting to minimize chargebacks and fraud losses.

Allows businesses to create and manage virtual and physical payment cards for use cases such as expense management and customer rewards. Enables businesses to create, manage, and distribute virtual and physical payment cards.

Key Features: Instantly generate virtual cards for online purchases or expense management. Issue physical Visa cards (white-labeled with your brand). Set spending limits, merchant controls, and real-time authorizations. Track and manage card usage via API.

Example Use Cases: Expense cards for employees (like Brex). On-demand gig worker payment cards. Rewards or cashback cards for loyalty programs

Treasury: Embedded banking-as-a-service, letting platforms offer financial accounts, ACH transfers, and more. A banking-as-a-service platform that lets platforms embed financial services like bank accounts, payments, and cash flow tools.

Key Features: Create FDIC-insured bank accounts for users (via partner banks like Goldman Sachs). Enable ACH transfers, wire transfers, and interest-earning balances. Integrated with Connect for seamless payouts and account controls. Ideal for B2B platforms, marketplaces, and neobanks.

Example Use Cases: Shopify offering business accounts to merchants. Platforms providing embedded accounts for freelancers or vendors.

POS hardware and software for in-person payment solutions, enabling seamless omnichannel experiences. A solution for in-person payments, providing both hardware and APIs for building custom POS systems.

Key Features: Supports chip, swipe, and contactless payments. Works with iOS, Android, and web apps. Fully integrated with Stripe’s online systems (omnichannel). Available hardware: Stripe Reader M2, WisePOS E, and BBPOS Chipper.

Ideal For: Retailers, restaurants, pop-up stores, service providers needing in-person transactions.

Tools to support recurring billing, subscriptions, and automated invoicing, ideal for SaaS businesses.

Key Features: Subscription plans with custom intervals, free trials, coupons, and metered billing. Smart retries and automated dunning for failed payments. Professional PDF invoices with embedded payment links. Integrates with QuickBooks, Xero, NetSuite. Support for tax collection (Stripe Tax), proration, and upgrades/downgrades.

Ideal For: SaaS businesses, service providers, agencies, and freelancers.

One of Stripe’s standout offerings is Connect. It powers marketplaces and platforms by handling complex money movement, compliance, and payout workflows. For example: Shopify uses Connect to pay out its merchants. Lyft leverages it to instantly pay drivers. Kickstarter relies on it to route funds from backers to creators. Upwork automates global freelancer payments and compliance.

With Connect, platforms can onboard users quickly, split payments, manage risk, and ensure tax and regulatory compliance with minimal overhead.

Stripe Connect is one of Stripe's most powerful products — it powers platforms and marketplaces by enabling them to onboard, verify, pay out, and manage third-party sellers, service providers, or freelancers, all while remaining compliant with local financial regulations.

Stripe Connect is a payments platform-as-a-service (PaaS) that allows businesses to: Onboard users (sellers, drivers, freelancers) easily. Accept and route payments between buyers and third parties. Split fees (take platform commission or charges). Handle payouts, including real-time, scheduled, or international payouts. Maintain KYC/AML compliance, tax reporting, and banking connections.

Enables merchants to receive payments via Shopify Payments (powered by Stripe Connect). Onboards merchants using Express accounts. Stripe handles KYC checks. Shopify can take a percentage of each transaction. Enables seamless payouts to merchants' bank accounts.

Pays drivers across the U.S. and Canada. Lyft uses Custom Connect accounts for full branding and user control. Stripe handles driver identity verification and compliance. Supports instant payouts to drivers via debit cards.

Crowdfunding platform needs to accept funds and disburse them to project creators. Stripe Connect collects pledges from backers. Funds are held until the funding goal is met. Stripe disburses funds to creators minus platform fees.

Freelancer marketplace for global talent. Onboards freelancers and clients. Collects client payments and automatically routes payments to freelancers. Manages global compliance and tax reporting (e.g., 1099 for U.S. freelancers).

Facilitates transactions between customers and shoppers/delivery personnel. Stripe Connect is used to collect customer payments and split them between Instacart and workers. Offers instant payouts for drivers via debit card using Stripe’s infrastructure.

Example: Workflow of Stripe Connect

1. Seller signs up → Stripe verifies identity (KYC).

2. Buyer makes purchase → Funds are collected.

3. Funds split → Stripe sends seller their portion, platform keeps fee.

4. Payout processed → Seller receives money (immediate or scheduled).

5. Platform dashboard → Monitor activity, block users, adjust settings.

Stripe operates in over 45 countries and supports 135+ currencies. Its clients include Amazon, Google, Zoom, Notion, and Salesforce. It has also opened major offices in Singapore, Dublin, Tokyo, and London, ensuring local compliance and support as it expands its global footprint.

Patrick and John Collison have always emphasized that Stripe’s mission is to “increase the GDP of the internet.” This means enabling more entrepreneurs to start businesses, empowering platforms to scale faster, and making global financial services accessible to all.

As it prepares for an eventual IPO and expands deeper into embedded finance, AI-powered fraud prevention, and financial infrastructure, Stripe is poised to remain at the forefront of fintech innovation.

From simplifying online payments to enabling complex global marketplaces, Stripe has redefined what financial infrastructure looks like in the digital era. Its continued innovation, developer-first mindset, and commitment to global accessibility make it a critical player in the future of finance. Whether you're a startup founder or an enterprise CTO, Stripe offers the tools to build, scale, and thrive in the internet economy.