Explore Indonesia's nickel industry outlook, government policies, and why investors are looking beyond mining into batteries, recycling, and green processing.

Explore Indonesia's nickel industry outlook, government policies, and why investors are looking beyond mining into batteries, recycling, and green processing.

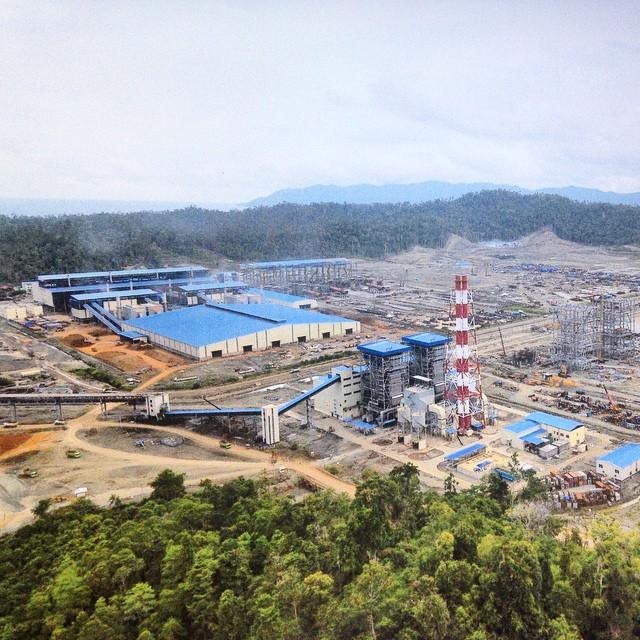

Image courtesy of Indonesia Business Post

Indonesia has emerged as the undisputed leader in the global nickel industry. Over the past decade, the country has transformed itself from a supplier of raw nickel ore into the world's most influential nickel-processing hub. Supported by government policies aimed at downstream industrialization, Indonesia now occupies a central position in the global supply chain for stainless steel, electric vehicles (EVs), and battery manufacturing.

While nickel prices have experienced periods of volatility due to increased production and global market fluctuations, long-term demand remains promising. As countries invest heavily in renewable energy, battery technology, and electrified transportation, nickel continues to be recognized as one of the most important strategic minerals of the 21st century.

Indonesia is one of the most important countries in the global nickel industry. In fact, it has transformed from a raw ore exporter into the world's dominant nickel producer and processor in less than a decade. Today, nickel is one of Indonesia's most strategic commodities, alongside coal, palm oil, and copper.

Nickel is used in: Stainless steel production (the largest market). Electric vehicle (EV) batteries. Consumer electronics. Aerospace components. Energy storage systems. As global demand for EVs and renewable energy grows, nickel has become a critical mineral for the energy transition.

Indonesia is The world's largest nickel producer. Home to the world's largest nickel reserves. Responsible for more than 60% of global nickel mine production. The largest supplier of nickel products used in stainless steel and EV battery supply chains. Production reached approximately 2.2–2.3 million metric tons annually, far exceeding competitors such as the Philippines, Russia, and Australia.

The Export Ban That Changed Everything. A major turning point came when the Indonesian government banned exports of unprocessed nickel ore. Force companies to process nickel domestically. Attract foreign investment. Create jobs. Increase export value through downstream industries. The policy triggered billions of dollars in investment in smelters and processing facilities, especially from Chinese companies. More than 60 smelters have been developed across the country.

Major Nickel Regions in Indonesia

Sulawesi. The heart of Indonesia's nickel industry. Morowali. North Morowali. Konawe. Kolaka. Maluku Islands. Important growing production centers. Key areas: Weda Bay and Halmahera. These regions host some of the largest nickel processing hubs in the world.

Indonesia wants to move beyond mining and become a complete EV battery manufacturing hub. The strategy includes: Nickel mining. Nickel processing. Battery materials. Battery manufacturing. Electric vehicle production. Major international investors from China, South Korea, and other countries have invested heavily in Indonesia's battery ecosystem.

Nickel has become one of Indonesia's largest export earners. Benefits include: Billions of dollars in export revenue. Increased foreign direct investment (FDI). Job creation in eastern Indonesia. Development of industrial parks and infrastructure. Stronger position in global critical mineral supply chains. The downstream strategy has significantly increased the value generated from Indonesia's mineral resources.

Challenges Facing the Industry

Falling Nickel Prices. Indonesia's rapid production growth has contributed to global oversupply, putting pressure on nickel prices.

Environmental Concerns. Critics point to: Deforestation. Waste disposal issues. Water pollution. Marine ecosystem impacts. High carbon emissions from coal-powered smelters. These issues have become increasingly important for global EV manufacturers and ESG-focused investors.

Dependence on Coal. Many nickel smelters rely on captive coal-fired power plants, making Indonesian nickel more carbon-intensive than some competing sources.

Dependence on Foreign Technology and Capital. A large share of Indonesia's processing sector has been developed with Chinese investment and technology, creating ongoing debates about long-term industrial independence.

The industry is entering a new phase: Growth is expected to slow from the explosive expansion seen since 2020. More focus will be placed on higher-value battery materials. Green energy-powered smelters are likely to become more important. Indonesia is expected to remain the world's dominant nickel supplier throughout the decade.

Indonesia's nickel industry is one of the country's biggest industrial success stories. By banning raw ore exports and encouraging domestic processing, Indonesia transformed itself from a commodity exporter into the center of the global nickel supply chain. The next challenge is balancing economic growth with environmental sustainability while moving further into EV batteries and advanced manufacturing. For investors, however, the opportunities in Indonesia's nickel industry are no longer limited to mining. Government regulations and market trends are reshaping the sector, creating new pathways for businesses seeking sustainable growth and higher-value returns.

Indonesia's decision to ban exports of unprocessed nickel ore fundamentally changed the industry's direction. Rather than allowing raw materials to leave the country, policymakers encouraged domestic processing and refining, attracting billions of dollars in foreign direct investment.

This strategy led to the rapid development of smelters, industrial parks, and downstream facilities across Sulawesi and Maluku. Major industrial hubs such as Morowali and Weda Bay have become globally recognized centers for nickel processing and manufacturing. The government's objective is straightforward: maximize economic value, create jobs, and establish Indonesia as a leading producer of battery materials and advanced industrial products. Today, investors entering the market are expected to contribute to this broader vision rather than focusing solely on raw material extraction.

Nickel's importance extends far beyond traditional mining. Historically, the metal has been used primarily in stainless steel production, which remains the largest source of global demand. Stainless steel is essential for infrastructure, construction, manufacturing, transportation, and consumer goods. However, the rise of electric vehicles has created a second major growth engine.

Many advanced EV batteries rely on nickel-rich chemistries that provide higher energy density and longer driving ranges. As governments and automakers worldwide pursue carbon-reduction goals, demand for battery materials continues to increase. In addition, renewable energy systems increasingly require large-scale energy storage solutions. Battery technologies used in these systems often depend on nickel and other critical minerals. This combination of industrial and energy-transition demand gives nickel a unique position within the global economy.

Government Regulations Are Shaping Investment Decisions

Indonesia's current regulatory environment clearly favors downstream investment. While mining remains important, the government has signaled that future growth should come from higher-value activities such as refining, battery materials, chemical processing, and advanced manufacturing.

Recent policy adjustments have made it more difficult to justify investments focused exclusively on intermediate products such as Nickel Pig Iron (NPI) and ferronickel. Instead, policymakers are encouraging the production of battery-grade materials and products that support Indonesia's ambitions in the EV sector. Current Indonesian Government Regulations for Nickel Companies, Businesses & Investors.

Indonesia's nickel sector is no longer just a mining business. The government is actively steering the industry toward downstream processing, battery materials, and strategic industrial development. Any investor entering the sector today must understand that Indonesia wants value-added production, not simply ore extraction.

Raw Nickel Ore Export Ban Remains in Force. One of the most important regulations is the continued prohibition on exporting unprocessed nickel ore. Companies are generally required to: Process ore domestically. Build or partner with smelters. Support downstream industries. This policy originates from Indonesia's mineral downstreaming strategy under the Mining Law and related regulations. Mining + domestic processing. Smelter development. Battery material production. EV supply chain investments.

New Smelter Investments Are Now More Restricted. A major policy shift occurred under Government Regulation No. 28/2025. Indonesia is limiting permits for new smelters that only produce intermediate products such as: Nickel Pig Iron (NPI). Ferronickel (FeNi). Nickel Matte. Mixed Hydroxide Precipitate (MHP). Instead, the government wants investors to move further downstream into: Battery precursor materials. Battery-grade nickel sulfate. EV battery components. Green industrial products. Finished manufacturing products. In 2026, Indonesia's preferred investor is no longer a basic smelter operator. The preferred investor is one that contributes to the battery and advanced manufacturing ecosystem.

Foreign Ownership Rules. Foreign investors can still enter Indonesia's nickel sector through a PT PMA structure. Nickel mining (KBLI 07295) remains open to foreign investment, including up to 100% ownership at the entry stage. However, mining companies remain subject to Indonesia's divestment rules. Divestment Requirement. Mining companies holding: IUP and IUPK, must gradually increase Indonesian ownership, reaching 51% domestic ownership by the tenth year of production. This is one of the most important considerations for foreign mining investors.

Annual RKAB Approval Requirement. The government has tightened control over production volumes. Mining companies must submit: RKAB (Work Plan and Budget). Production targets. Sales projections. Since late 2025, RKAB approvals are generally valid for one year instead of three years. The government can: Control national nickel output. Manage oversupply. Influence market stability. Monitor environmental compliance more closely.

Environmental Compliance Is Becoming More Important. Indonesia has significantly increased environmental scrutiny of mining and processing operations. Key requirements include: Environmental Impact Assessment (AMDAL). Mine reclamation plans. Post-mining restoration guarantees. Waste management systems. Water treatment facilities. Air emission controls. Companies that fail to comply face permit suspensions, sanctions, or operational restrictions. Environmental performance is becoming increasingly important as Indonesia seeks to attract global EV manufacturers and ESG-focused investors.

Priority for Downstream Projects. Recent amendments to mining legislation favor projects that create domestic value. Priority is increasingly given to companies that: Build processing facilities. Create industrial jobs. Support battery manufacturing. Contribute to strategic downstream industries.

New Export Governance Framework. The government has introduced a new strategic commodity export management system involving state oversight. Some nickel-related products, particularly ferroalloys, may be subject to increased reporting and state-supervised export procedures. However, Nickel Pig Iron (NPI) has been specifically exempted from certain centralized export requirements announced in 2026. This area is evolving and investors should monitor further implementing regulations. Indonesia's government is clearly signaling that the future lies in battery materials, advanced refining, and integrated industrial ecosystems rather than commodity nickel production alone.

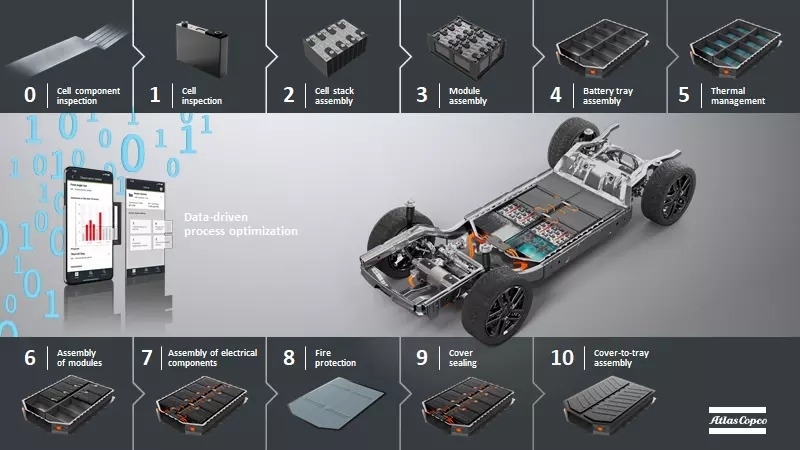

Battery Materials Platform (Highest Potential). Nickel Mine → HPAL Processing → Nickel Sulfate → Cathode Materials → Battery Industry. Indonesia is actively encouraging: Nickel sulfate. Battery precursors. Cathode materials. Battery cell manufacturing, while restricting new investment in lower-value intermediate products. Investment Size: US$500 million–3 billion+. Typically requires strategic partners from China, South Korea, Japan, or Europe. Potential Partners: Huayou Cobalt. LG Energy Solution. EcoPro. CATL. Highest long-term margins. Strong government support.

Green Nickel Industrial Park (My Favorite Long-Term Model). Instead of owning only a mine: Acquire: Mining concessions. Processing facilities. Renewable energy assets. Industrial land. Then lease facilities to: Battery companies. Chemical manufacturers. EV component manufacturers. The global market increasingly wants: ESG-compliant nickel. Low-carbon nickel. Traceable supply chains. Investor pressure is increasing around environmental standards and responsible mining. Indonesia Battery Corporation ecosystem. Morowali-style industrial zones. Weda Bay-style integrated parks. Recurring income from: Land lease. Utilities. Processing. Logistics. Port operations. This often becomes more profitable than mining itself.

Nickel Recycling Business. Recover nickel from: EV batteries. Consumer electronics. Industrial batteries. Governments worldwide are pushing: Circular economy. Battery recycling. Critical mineral security. By 2035, battery recycling could become one of the fastest-growing segments of the nickel value chain. Investment Range: US$10–200 million. Advantage: Lower environmental risk than mining.

High-Purity Nickel Chemicals. Produce: Nickel sulfate. Nickel powder. Specialty nickel chemicals. Plating chemicals. The market is broader than EVs. Customers include: Aerospace. Electronics. Semiconductors. Defense. Chemical industries. Experts increasingly recommend diversification beyond battery-only products because battery technology continues to evolve.

Strategic Mining + Processing JV. Business Model: Own: Nickel mine (30–49%). Processing plant (30–49%). Partner with: Foreign technology provider. Battery manufacturer. State-linked Indonesian partner. Indonesia's regulations and divestment framework make partnerships increasingly important. This reduces: Political risk - Technical risk - Financing risk. Produces: Nickel Pig Iron

Mine → HPAL → Nickel Sulfate → Cathode Materials

This is the direction Indonesia is explicitly encouraging through its downstream industrial strategy and battery ecosystem development plans. The Most Attractive Opportunity for a New Investor Today. The best risk-adjusted opportunity is likely battery-grade nickel sulfate and related chemical processing, rather than mining alone. It aligns with government priorities, captures more value per ton of nickel, attracts strategic partners, and positions the business within the global EV and energy-storage supply chain.

The Rise of Battery-Grade Nickel

One of the most promising segments of the industry is battery-grade nickel processing. Rather than selling ore or basic processed nickel products, companies can generate significantly higher value by producing materials used directly in battery manufacturing. Nickel sulfate, precursor materials, and cathode components are becoming increasingly important as global EV production expands.

Major automotive manufacturers and battery producers are actively seeking secure and reliable sources of these materials. Indonesia's vast nickel reserves, combined with growing processing capacity, place the country in a favorable position to serve this demand. For investors with access to technology, capital, and strategic partnerships, battery materials represent one of the most compelling opportunities within the nickel value chain.

Another trend attracting attention is the development of integrated industrial parks. Rather than operating a standalone mine or processing facility, some investors are building ecosystems that combine mining, refining, logistics, utilities, and manufacturing. Industrial parks create opportunities to generate recurring revenue through land leases, energy supply, port services, warehousing, and infrastructure management.

As more battery manufacturers, chemical producers, and advanced material companies establish operations in Indonesia, demand for well-developed industrial zones is expected to increase. This approach can also reduce exposure to commodity price fluctuations because revenue is generated from multiple business activities rather than a single product.

Green Nickel Could Become the Next Competitive Advantage

Environmental considerations are becoming increasingly important across global supply chains. Automotive manufacturers, institutional investors, and consumers are paying closer attention to carbon emissions, environmental management, and sustainability practices. As a result, the concept of "green nickel" is gaining momentum.

Producers that utilize renewable energy, reduce emissions, improve waste management, and demonstrate responsible mining practices may gain preferential access to premium markets.

For Indonesia, this presents both a challenge and an opportunity. Many existing nickel operations rely heavily on coal-powered energy sources. However, future projects that integrate solar, hydropower, geothermal, or other renewable energy solutions could differentiate themselves in the marketplace. Investors who prioritize sustainability today may be better positioned to meet future customer expectations and regulatory requirements.

Battery Recycling Is an Emerging Opportunity

While mining continues to dominate the industry, battery recycling is becoming an increasingly attractive business segment. As electric vehicle adoption grows, millions of batteries will eventually reach the end of their useful life. Recovering nickel and other valuable minerals from these batteries offers significant economic and environmental benefits.

Battery recycling supports circular economy initiatives, reduces dependence on new mining projects, and helps secure long-term supplies of critical materials. Globally, many analysts expect battery recycling to become a multi-billion-dollar industry over the next decade.

Indonesia's ambitions to become a major battery manufacturing hub could create additional opportunities for local recycling operations and supporting industries. The Future of Nickel: Global Outlook and Investment Prospects. Nickel remains one of the world's most important strategic minerals because it sits at the intersection of two massive industries: Stainless steel manufacturing. Electric vehicle (EV) and energy storage batteries. While the nickel market is currently facing oversupply and lower prices, the long-term outlook remains positive due to increasing demand from electrification, renewable energy, and industrial development.

According to industry forecasts from organizations such as the International Energy Agency and major mining companies, global nickel demand is expected to continue growing through 2040. Main Demand Drivers:

Electric Vehicles (EVs). Nickel-rich batteries offer: Higher energy density. Longer driving range. Better performance. Battery chemistries such as NMC (Nickel-Manganese-Cobalt) and NCA (Nickel-Cobalt-Aluminum) require significant amounts of nickel. Major EV manufacturers continue to rely on nickel-based batteries for premium and long-range vehicles, even as some manufacturers adopt LFP batteries for lower-cost models.

Energy Storage Systems. Large-scale renewable energy projects require battery storage systems. As solar and wind installations expand globally, demand for battery materials, including nickel, is expected to increase.

Stainless Steel. Despite the excitement around EVs, stainless steel still accounts for most nickel consumption globally.

Growing urbanization and infrastructure development in: India. Southeast Asia. Africa. Middle East will continue supporting stainless steel demand.

Battery-Grade Nickel. The highest-growth segment is not mining itself but producing: Nickel sulfate. Cathode materials. Battery precursors. These products command significantly higher margins than raw ore.

Green Nickel. Many automotive manufacturers increasingly require low-carbon nickel. Companies that can produce nickel using: Hydropower. Solar power. Geothermal energy, may gain access to premium markets.

Recycling. Battery recycling is expected to become a multi-billion-dollar industry. Recovered nickel from used batteries can reduce reliance on new mining while supporting sustainability goals.

Investment Outlook. The most attractive opportunities are likely to be:

High Potential: Battery-grade nickel refining - EV battery materials - Nickel recycling - Green nickel production - Industrial parks linked to battery manufacturing

Moderate Potential: Traditional nickel mining - Stainless steel-focused nickel operations

Higher Risk: Pure ore-export businesses - High-cost mining projects without downstream integration

The next decade will likely see nickel transition from being primarily a stainless steel metal into a critical energy-transition mineral. For Indonesia specifically, the greatest value will not come from mining more nickel ore, but from moving further downstream into: Battery materials. Battery manufacturing. EV production. Battery recycling. Renewable-energy-powered processing. If Indonesia succeeds in these areas, nickel could become one of the country's most important industrial growth engines through 2040, much like oil was for some economies in previous decades.

Despite its strong potential, the nickel sector is not without risks. Global nickel prices remain vulnerable to oversupply. Indonesia's rapid expansion has increased production volumes significantly, placing pressure on international markets. Technology trends also require careful monitoring. While many EV batteries use nickel-rich chemistries, some manufacturers have adopted alternative battery technologies that require little or no nickel.

Environmental compliance is becoming more stringent, both domestically and internationally. Companies must invest in responsible practices and maintain strong relationships with regulators, local communities, and customers. Finally, successful projects often require substantial capital, technical expertise, and long-term planning. Investors entering the sector should view nickel as a strategic industrial investment rather than a short-term commodity play.

The Future Belongs to Value Creation

Indonesia's nickel story is no longer simply about extracting minerals from the ground. The next phase of growth will be defined by processing, innovation, manufacturing, sustainability, and integration into global supply chains.

For investors, the greatest opportunities are likely to emerge from businesses that create value beyond mining. Battery materials, industrial infrastructure, recycling, specialty chemicals, and green processing solutions all offer pathways to participate in one of the world's most important industrial transformations.

As global demand for critical minerals continues to rise, Indonesia remains uniquely positioned to shape the future of the nickel industry. The question for investors is no longer whether nickel has a future, but where in the value chain they can create the most value.